The David vs. Goliath Technology Gap

Picture this: You’re sitting in your Study Group, listening to market leaders talk about their impressive digital transformations. They showcase AI-powered analytics, automated workflows, and sophisticated logistics systems that seem to run like clockwork. They are already much larger than your company but seem to be able to scale with minimum effort. As a smaller company owner or manager, you might feel that familiar pang of technology envy – wondering if you’ll ever be able to compete with these tech-savvy giants. More importantly, you might be hearing that voice in your head asking, “How can I be competitive at my current size?”

This feeling is more common than you think. In peer groups and trade shows across the refined fuels market, smaller companies often leave meetings feeling overwhelmed by the technological capabilities of their larger counterparts. The assumption that advanced technology is only for companies with deep pockets and dedicated IT departments has created a dangerous myth that keeps smaller businesses from reaching their full potential.

The reality is far more encouraging: today’s technology landscape offers unprecedented opportunities for small and medium-sized businesses to punch above their weight class. The key isn’t matching your larger competitors feature-for-feature but rather implementing the right technology solutions strategically and efficiently.

The Modern Advantage: Why Smaller is Sometimes Better

Smaller companies actually possess several advantages when it comes to technology adoption:

Agility and Speed: While large corporations often struggle with bureaucratic approval processes and complex legacy systems, smaller companies can implement and adapt new technologies quickly. A decision that might take months in a large organization can happen in days or weeks in a smaller company.

Focused Implementation: Rather than trying to solve every problem at once, smaller companies can target specific pain points with precision. This focused approach often leads to higher success rates and better returns on investment.

Direct Leadership Involvement: In smaller organizations, decision-makers are often directly involved in daily operations. This means technology choices are made by people who understand the real challenges and can see immediate benefits.

Lower Change Management Complexity: Getting a team of 15 people to adopt a new system is significantly easier than managing change across hundreds or thousands of employees. It’s also generally easier to step into change from no technology rather than replacing technology that already has a heavy investment of time and dollars, even if that existing technology is no longer effective.

Getting Started: Strategies to Consider

1. Audit Your Current State

Before investing in any new technology, take inventory of what you already have. Many small companies discover they’re underutilizing existing tools or paying for overlapping services. Create a simple spreadsheet listing:

- Current software and systems

- Monthly/annual costs

- Primary users and usage frequency

- Integration capabilities

- Pain points and limitations

This audit will help you identify gaps, redundancies, and opportunities for consolidation.

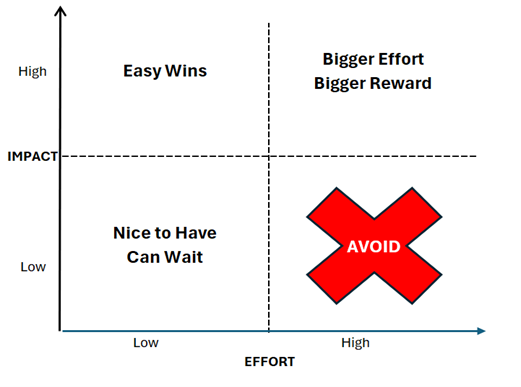

2. Prioritize Based on Impact and Effort

Not all technology investments are created equal. Use a simple matrix to evaluate potential solutions:

- High Impact, Low Effort: Quick wins that provide immediate value

- High Impact, High Effort: Strategic investments worth planning for

- Low Impact, Low Effort: Nice-to-have features that can wait

- Low Impact, High Effort: Avoid these entirely

Focus your limited resources on solutions that will deliver the biggest bang for your buck. In the fuel/c-store space this usually involves bottom-line numbers:

- Lower laid-in fuel costs

- Higher operational efficiency in trucking fleets

- Better, faster, more accurate invoicing (time cost of money)

- Higher fuel margins through competitive analysis tools

- Higher in-store volume through promotion or loyalty technology

- Sales enablement tools to maximize new revenue

3. Start with the Right Business Functions

Rather than trying to modernize everything at once, begin with your most critical business processes.

- Where is the sharpest pain?

- What prevents you from scaling your business or increasing margins?

- What technology do you have that is being sunsetted?

4. Take Charge

Are you waiting for John or Jane to retire before implementing technology because you don’t want to rock the boat and maybe John doesn’t want change or Jane says she’ll quit if she has to learn a new system? It’s time to take charge and manage the change that needs to occur. Even the most seasoned employees get onboard when their jobs become less stressful with the right technology tools and processes.

Smart Technology Strategies for Resource-Constrained Organizations

1. Embrace Cloud-First Solutions

Cloud-based software eliminates the need for expensive hardware, IT maintenance, and complex installations. Software-as-a-Service (SaaS) solutions offer:

- Predictable monthly costs instead of large upfront investments

- Automatic updates and security patches

- Scalability that grows with your business

- Access from anywhere with an internet connection

2. Leverage Experts

Many organizations will retain industry-specific consulting services to help implement new technology and reduce the internal labor demand.

3. Let the Vendor do the Heavy Lifting

New technology will inevitably require implementation. Good vendors will have teams of industry veterans who understand your business, have many successful implementations to draw from, and will be more efficient than if you try to do the implementations with minimal vendor support, i.e., you try to save a few dollars.

While this method does raise initial costs, you should consider the intangible benefits of not delaying implementation or pausing implementations because you have other priorities/emergencies that arise in the business.

Implement Gradually

A delayed implementation can be costly, but a strategically phased deployment can spread costs over time and reduce implementation stress. A typical progression might look like:

- Months 1-3: Core functionality

- Months 4-6: No activity

- Months 7-12: Additional toolsets/features that enhance the core functionality

- Year 2: Bring on the remainder of the full suite of tools

This is a similar strategy that larger organizations employ geographically, rather than functionally. They might implement technology by markets, countries or continents individually before moving on to the next phase.

Managing Risks

1. The People Factor

Technology success depends more on user adoption than technical features. Involve your team in the selection process and provide adequate training. Consider these strategies:

- Choose intuitive, user-friendly solutions over feature-rich but complex ones

- Designate technology champions within your team

- Provide hands-on training, not just documentation

- Check in with your team regularly as you implement to gather feedback or course-correct as needed.

2. Budgets

Technology costs can spiral quickly if not carefully managed. Protect yourself by:

- Setting a budget before evaluating options. Today’s vendors normally have scaled pricing by volume (users, sites, trucks, etc.) AND feature sets, so getting a price early in your evaluation process can be difficult.

- Signing an NDA but sharing openly about your goals/restrictions. A good vendor will work with you to prioritize needs and try to work within your parameters.

- Building in a 20% contingency for unexpected costs

3. Security Concerns

Smaller companies often assume they’re not targets for cybercriminals, but they’re actually attractive because they typically have weaker security measures. When evaluating solutions:

- Verify security certifications (SOC 2, ISO 27001)

- Ensure data encryption in transit and at rest

- Understand data backup and recovery procedures

- Implement multi-factor authentication wherever possible

- Train employees on security best practices

4. Vendor Quality

You joined a peer group for a number of reasons, one of which might be that you get to share experiences with vendors. In a tightly networked industry such as this, peer references will carry significant weight in your technology evaluations.

- Perfection doesn’t exist, but ensure that you are comfortable with the vendor, and that they will be responsive if something were to go wrong.

- Does the vendor invest in their products with regular updates and enhancements?

- Does the vendor share their future roadmap with their customers?

Measuring Success and ROI

Technology investments should deliver measurable benefits. Track key performance indicators such as:

- Time saved on routine tasks

- Improved customer response times

- Reduced errors and rework

- Increased sales or customer retention

- Employee productivity and satisfaction

- Better equipment utilization

Set baseline measurements before implementation and review progress regularly. And if you have any turnover in your organization, train the new employees fully on your technology so you don’t lose ROI by limited use of your solution.

The Competitive Reality

Technology levels the playing field more than ever before. A small business using the right tools can be just as attractive to a customer as a larger organization.

Your customers don’t care about the size of your IT department; they care about their experience with your business. A responsive, small company with smart technology and streamlined processes can deliver accurate and reliable services.

Moving Forward: Your Action Plan

- Assess your current state: Complete a business process/technology review within the next 60-90 days.

- Identify quick wins: Choose one high-impact, low-effort improvement to implement immediately.

- Create a roadmap: Plan your technology adoption over the next 12-18 months.

- Start small: You don’t have to implement everything all at once.

- Build internal support: Get your team involved in the process early.

- Monitor and adjust: Regularly review and optimize your technology stack.

Conclusion

The days of technology being exclusively for large organizations are over. Today’s small businesses have access to tools that would have been impossible to afford just a decade ago. The question isn’t whether you can afford to invest in technology, it’s whether you can afford not to.

Your larger competitors may have bigger budgets, but you have advantages they may not: speed, focus, and the ability to rapidly implement solutions that directly address your specific challenges. By approaching technology strategically and implementing solutions selectively, you can build a competitive advantage that rivals companies many times your size.

The “Joneses” you’re trying to keep up with may have started their technology journey earlier, but that doesn’t mean you can’t catch up or even surpass them. With the right strategy, realistic expectations, and smart implementation, your small company can leverage technology to compete with anyone in your industry.

The future belongs to businesses that can adapt quickly and serve customers effectively – size is just a number. Your path forward starts with a single step, and there’s no better time to take it than now. And if you are strategic and select the right technology, you might end up being one of the dominant organizations that others seek to emulate.