When a reliable customer’s payment habits begin to slip, it is a signal you can’t afford to ignore. A variety of factors — new ownership, management changes, divorce, loss of a key customer or broader economic pressures — can quickly turn a once dependable account into a potential credit risk.

When you start feeling uneasy about a customer’s financial stability:

Gather updated information.

- Pull a fresh credit report and compare the updated information with your initial credit report.

- Request current financial statements, and if you have previously received their financials, compare the KPI trends.

- Talk to your drivers who might be delivering onsite and reassess the credit limit based on the most recent data.

If the customer’s recent payment habits and purchasing needs no longer align with the historically approved credit line, it’s time for a direct, honest conversation with the customer. Explain the concerns, outline the revised terms, and clarify what the customer must do to strengthen the relationship moving forward.

If red flags continue to appear:

Consider reinforcing your position by requesting collateral.

Real estate, Letters of Credit, Personal Guarantees, deposits or unencumbered assets can provide valuable protection.

There is no doubt these tools are not always easy to secure in longstanding relationships, and it can feel like locking the barn door after the horse has escaped, but they remain negotiating tools and potentially important safeguards when risk is rising. It’s a good reminder to ask for collateral at the beginning of a relationship for any customer who does not present an expected level of credit strength.

When red flags are raised, be prepared to negotiate and think creatively.

One effective approach is to ask the customer to pay down open balances that are not yet due, reducing your exposure. You can continue providing product — such as fuel deliveries — until the credit cap is reached again, at which point another payment is required.

Another option is to establish a routine payment schedule, such as weekly Friday payments, to keep credit risk under control.

These payment-habit compromises allow the customer to continue receiving product while preventing the supplier from carrying an unsustainable credit overage. Be prepared to work with your customer while they potentially work out of a difficult stage of business.

Sometimes a customer who was once considered “good” gradually slips into a different category. Underperforming accounts often consume disproportionate time and attention, and hoping the situation improves on its own is not a proactive strategy.

When a customer who owes you money begins showing signs of distress, early action is essential.

Bottom line, not every customer is a good customer for life.

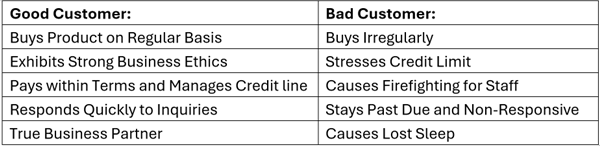

What is the definition of a good customer?

Protecting the integrity of your petroleum company is about cultivating, managing and partnering with customers that offer a secure platform for the relationship.