When you are evaluating a brand change, renewal, or debranding decision, the conversation almost always starts with fuel cost, signing bonuses, and brand incentives. Those matter. But there is another line item that rarely gets the same scrutiny and can quietly cost you just as much: credit and debit card processing fees.

Though there are many pricing programs, gas stations typically see two types of fee programs:

- Tiered: Branded programs require you to process cards through the oil company’s designated network using tiered pricing.

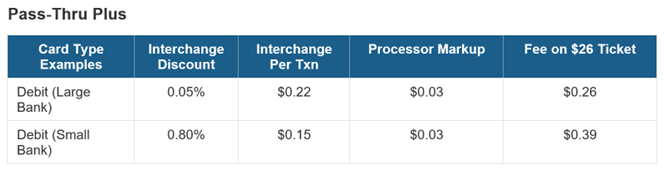

- Pass-Thru Plus: Unbranded stations get to choose their own processor, and that usually means access to interchange-plus pricing (aka Pass-thru Plus), where you pay the actual interchange cost set by Visa, Mastercard, and the other networks plus a small, transparent processor markup.

The difference between those two models is where the hidden money lives.

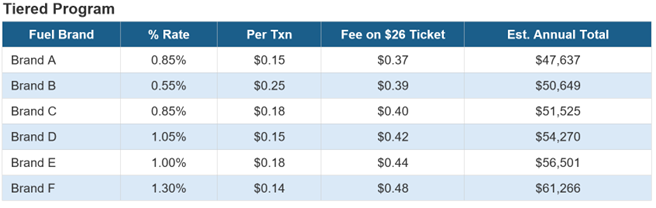

Debit Fees: Where the Biggest Dollars Hide

Debit transactions typically make up the largest share of a c-store’s card volume, so even small rate differences here get multiplied across a massive base. And the rate differences across brands are not small.

Look at pin debit rates across several major oil brands. The annual totals below are based on a store processing roughly 130,000 debit transactions and $3.3 million in debit volume per year:

The spread between the lowest and highest branded program is over $13,000 per year on debit alone, and none of those rates tells you what interchange actually costs.

With interchange-plus pricing, a processor charges $0.03 per transaction above interchange with no percentage markup at all. On a $26 average debit ticket, you see the interchange cost, you see the $0.03, and that is the entire fee. No tiers, no guessing.

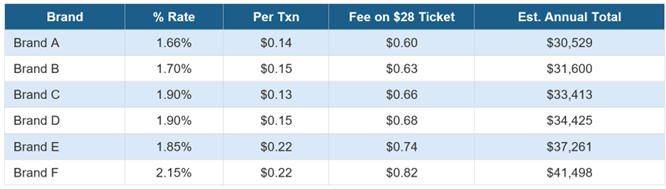

Visa and Mastercard Credit: A Wide Spread

Credit card rates show even wilder variation across branded programs. Consider Visa credit rates from several major brands, with annual totals based on roughly 50,000 transactions and $1.4 million in Visa credit volume:

The gap between the lowest and highest branded Visa rate is nearly half a percent, plus a $0.09 difference in per-transaction fees. That translates to roughly $11,000 per year in additional cost on Visa alone. Mastercard rates show a similar range.

Under interchange-plus, a Visa credit transaction at a $28 average ticket carries an effective interchange rate of roughly 1.80%. Add a flat $0.03 processor markup and that is your total cost. Compare that to 2.15% + $0.22 from the most expensive branded program, and the per-transaction savings are obvious.

Your Ticket Size Changes the Math

Here is something most brand comparisons completely overlook: your effective interchange rate changes based on your average ticket size. A store averaging $26 per debit transaction has a meaningfully different effective rate than one averaging $40. That effective rate can drop from approximately 1.52% at a $26 ticket down to 0.92% at $40. That is a 60 basis point swing on your highest-volume card type.

Branded tiered pricing does not account for this. You pay the brand’s fixed tier rate regardless of your ticket size. Under interchange-plus, you benefit directly when your ticket increases because the effective interchange cost drops and the processor’s flat per-transaction fee stays the same. If fuel prices push your average ticket higher, that savings flows straight to your bottom line instead of padding the brand’s margin.

EBT: The Overlooked Gotcha

Not every branded program supports EBT processing. If your brand’s designated processor does not handle EBT, you are stuck finding and paying a second processor just to run those transactions. That means a separate account, a separate statement, and additional fees and complexity for something that should be straightforward. For stores with meaningful EBT volume, the hassle and cost of maintaining a second processing relationship adds up quickly.

Before signing or renewing, confirm whether your branded program supports EBT natively. If it does not, factor that into your total cost of doing business with the brand.

What Tiered Pricing Actually Hides

The fundamental problem with branded tiered pricing is not just that it tends to cost more. It is that you cannot see what you are paying for. When a brand quotes 1.90% + $0.15 on Visa, that single number bundles interchange, brand overhead, program costs, and processor margin together. You have no way to know whether interchange represents 70% or 90% of that rate, and no way to know how much margin the brand is extracting from each swipe.

Interchange-plus pricing eliminates that problem. Interchange passes through at cost. The processor’s markup sits right next to it. If interchange drops for any reason, you see the benefit immediately. Under tiered pricing, the brand keeps the difference.

The $100,000 Difference

Signing bonuses and brand incentives get all the attention during negotiations. Processing fees should get equal weight, because they run every single day for the life of the deal. On a multi-store portfolio, the annual difference between tiered and interchange-plus pricing can easily reach six figures. The savings from better processing rates do not show up as a one-time check. They compound year after year, across every transaction, at every store.

Before your next brand decision, pull your transaction data, break it out by card type, and compare what you are paying now against what interchange-plus would cost. The numbers usually speak for themselves.

Want to see what your stores would save?

Send us your transactions by card type and we will run a side-by-side comparison against your current brand or processor. No cost, no obligation. Just the numbers.