By Dr. David Nelson

The April 2026 U.S. jobs report offers a portrait of an American labor market that continues to defy the most pessimistic forecasts while simultaneously resisting any return to the dynamism of the post-pandemic hiring boom. The number of jobs created in April was well above what was forecast, but the deeper picture is one of a labor market finding its new, more modest equilibrium.

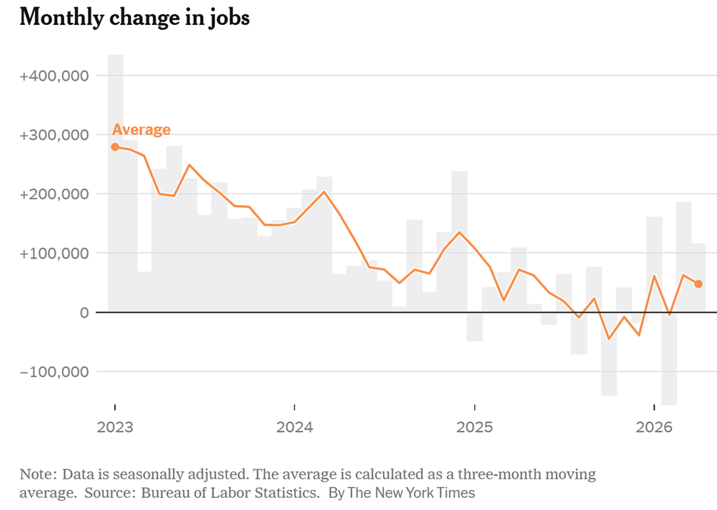

Nonfarm payrolls rose by a seasonally adjusted 115,000 in April, down from the 185,000 created in an unusually strong March, but well ahead of the forecast of around 55,000. Private payrolls led the way, adding 123,000 jobs — significantly above the predicted 75,000. Coming into the report, anxiety was running high: geopolitical instability, elevated oil prices tied to the Iran conflict (gas prices up $1.55 per gallon since the war began), and lingering uncertainty about monetary policy.

Healthcare led job creation, adding 37,000 new positions, with transportation, warehousing, and retail trade also contributing gains. Healthcare has become the most consistent engine of American job growth, driven by demographic demand that is largely impervious to economic cycles. It is a sector that can be counted on to pad the monthly numbers even when the broader economy stumbles.

The manufacturing sector told a less cheerful story. Manufacturing unexpectedly shed jobs in April, a reminder that goods-producing industries remain under pressure from elevated borrowing costs and uncertain trade conditions. Federal government employment also contracted, with the federal government’s workforce shedding 9,000 jobs for the month. The ongoing reduction in the federal workforce, a trend that has persisted across several reports, reflects deliberate policy choices and continues to be a quiet drag on the headline totals.

As we look at job growth by sector longer term the biggest sectors for job growth since 2022 were: health care and social assistance up 3.6 million, leisure and hospitality up 1.6 million, and construction up 726,000. Two sectors experienced declines: information technology, which went down 211,000 and Federal government down 214,000. Retail trade and manufacturing saw small increases of 37,700 and 32,000, respectively.

Unemployment Holds Steady, But Context Is Everything

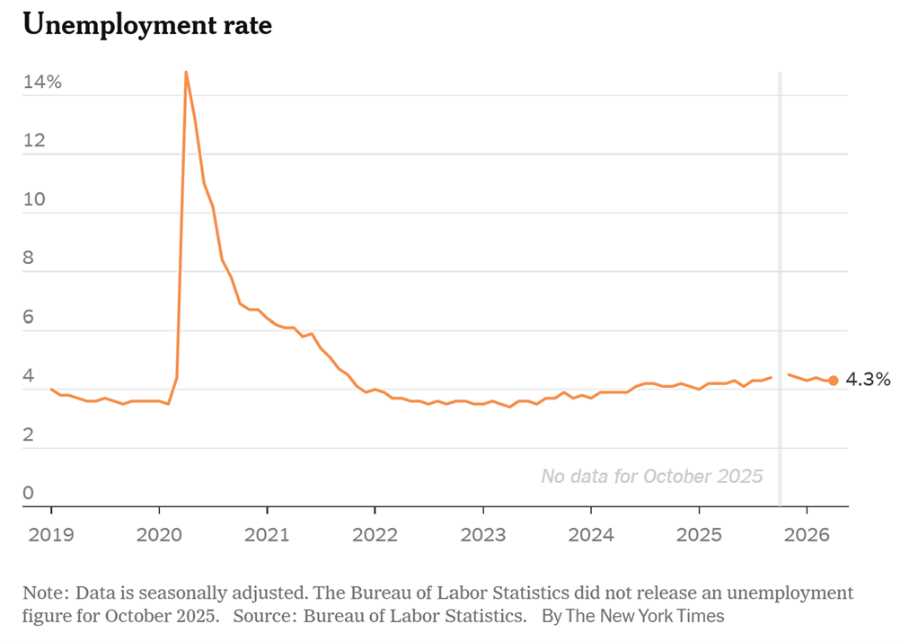

The official unemployment rate remained unchanged at 4.3 percent and optimists point to its stability as evidence of a resilient economy. Skeptics note that this masks a more complicated story. The March unemployment rate was 4.26% which rounds up to 4.3% and the April unemployment rate was 4.34% which rounds down to 4.3% so in actuality the unemployment rate rose .08% month over month. What can be said is that the trajectory of the unemployment rate has been unusual over the past few years, rising incredibly slowly (see chart). The unemployment rate for black workers rose from 7.1% to 7.3% and is the more than double the unemployment rate for white workers at 3.7%.

The labor force participation rate stood at 61.8 percent, with little change in April, and both that measure and the employment-population ratio edged down over the year. Meanwhile, the number of people who are not in the labor force who currently want a job held at around 6.1 million — individuals not counted as unemployed because they were not actively seeking work. These figures suggest that the official unemployment rate, while stable, does not fully capture the slack in the labor market. A broader measure of unemployment, which includes people employed part time for economic reasons as well as those who would like a job but have been discouraged from looking, sits at 8.2%.

Wages: A Relief for Inflation Watchers

One of the more consequential details in the report concerns wage growth. Average hourly earnings increased 0.2% for the month and 3.6% on an annual basis, coming in below expectations of 0.3% and 3.8%, respectively. For the Federal Reserve, which has been navigating a delicate balance between cooling inflation and avoiding a hard landing, this is welcome news. Wage moderation reduces the risk that labor costs will re-ignite price pressures.

Ellen Zentner, chief economic strategist at Morgan Stanley Wealth Management, noted that the solid jobs data leaves the Fed in a familiar position — watching and waiting, focused on inflation. She observed that rate cuts remain unlikely in the near term, but that the absence of inflationary signals in the report should quiet speculation about a potential hike. The April jobs report ratified the Fed’s view that it can afford to hold rates steady at a range of 3.5-3.75% as it contends with an uncertain economic backdrop.

The Bigger Picture: Solid but Slow

The 12-month average for job creation stands at just 22,000 — and excluding healthcare, the economy has seen a net loss of jobs over that stretch. That is a sobering figure, and it underscores just how much of the labor market’s apparent health rests on a single sector.

Economists have described the current environment as a “low fire, low hire” dynamic that has prevailed for the past two years. Workers who have jobs are keeping them; companies are not laying off in large numbers, but they are not staffing up aggressively either. It is a labor market in stasis — stable, but not generative.

The April 2026 jobs report, then, is neither a cause for alarm nor for celebration. It is evidence that the American labor market has found a lower gear and is holding it — resilient in the face of real headwinds, but no longer the growth engine it once was. For workers, policymakers, and investors alike, the challenge ahead is determining whether this steady-state is a plateau or a precursor to something more turbulent.