The 2025 Study Groups petroleum marketing financial results are in the books. Below we look at how four distinct business models performed against one another and the national average. Return on Capital Employed (ROCE) tells us which segments are generating the best returns, but the real story lies beneath that headline number: in gallons moved, margins earned, and the expense structures that determine how much of a company’s gross profit survives to the bottom line.

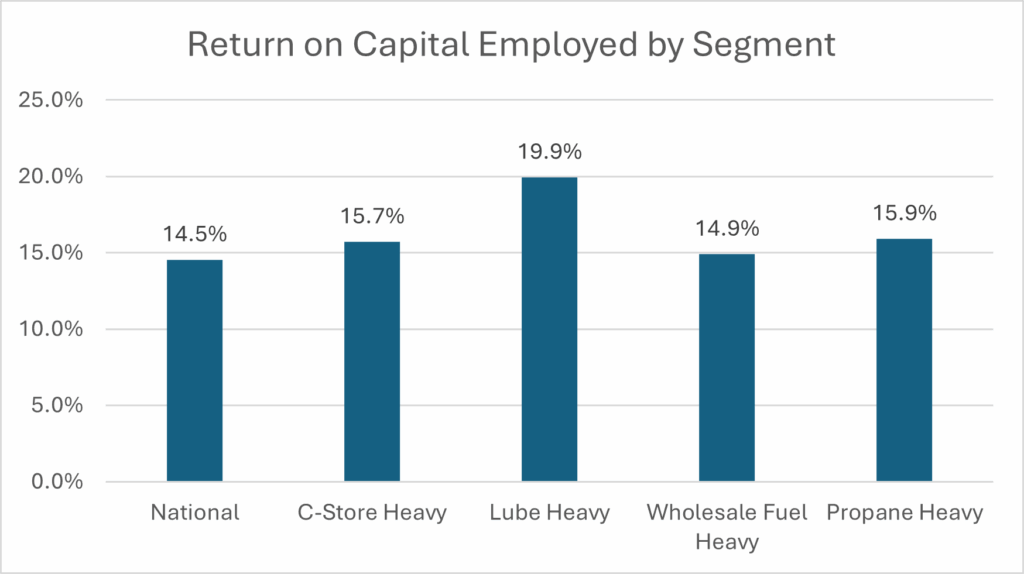

The four petroleum business models compared are C-Store Heavy Firms (29 firms in the sample), Lube Heavy Firms (20 firms), Wholesale Fuel Heavy Firms (10 firms), and Propane Heavy Firms (7 firms). All data is from the Study Groups database. Figure 1 lists their Return on Capital Employed for 2025.

Figure 1

The Standings

Lube Heavy Firms leads all segments with a ROCE of 19.9%, a full 5.4 percentage points above the national average of 14.5%. Propane Heavy Firms claims second at 15.9%, followed closely by C-Store Heavy Firms at 15.7%. Wholesale Fuel Heavy Firms finishes last at 14.9%, barely clearing the national average. All four business segments generated ROCE higher than the national average, indicating firms concentrated on one segment of the industry performed better than more full line firms with multiple petroleum marketing business lines. All four segments saw ROCE decline year-over-year, but the magnitude of those declines varied.

The Winner: Lube Heavy Firms

Lube Heavy Firms’ excellent 19.9% ROCE was aided with margins expanded by a blended CPG margin increase of +1.30 and volume growth of 8.9%, driven by a nearly 500,000-gallon increase in oils and greases for the average firm, a meaningful jump in diesel exhaust fluid volumes, and growth across multiple product lines.

These gains translated into gross profit dollar growth of 10.3% year-over-year, the strongest of any segment. Adjusted EBIT grew by 3.6%, keeping Lube Heavy Firms among only two segments (alongside C-Store Heavy Firms) to show any improvement. Despite these gains, Lube Heavy Firms’ ROCE still fell by 1.1 percentage points, the second-mildest decline but a decline, nonetheless.

Capital employed grew at a faster pace than both gross profit dollars and adjusted EBIT with an 11.2% increase, initiating an initial low return on that capital employed.

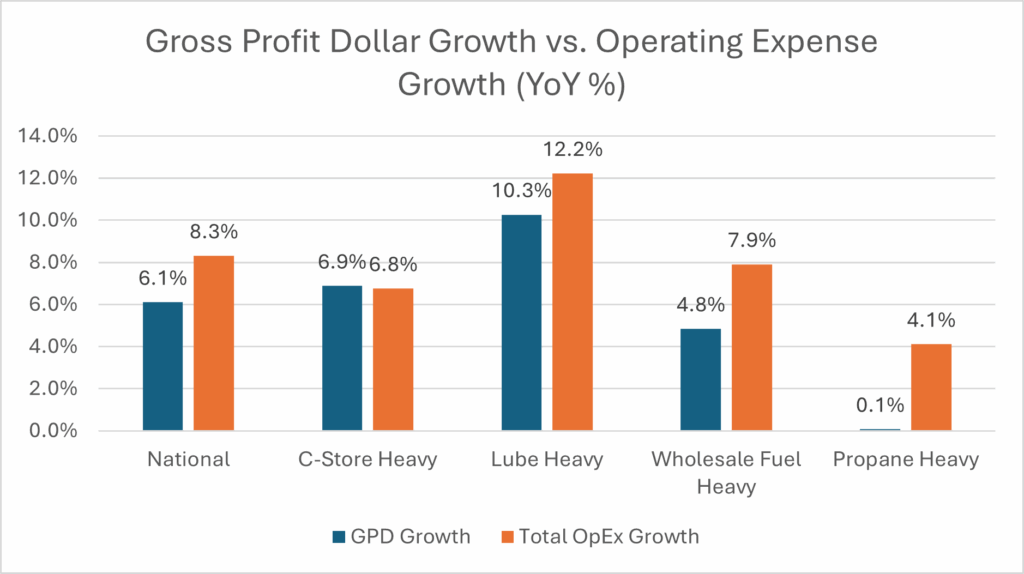

Expense growth also outpaced the robust gross profit growth with total operating expenses rising 12.2%, versus the 10.3% growth in gross profit dollars. The pain was concentrated in payroll, where payroll dollars increased 12.5% year-over-year. The dreaded “All Other” expenses increased 38.3% as well. These are the costs of a growing, labor-intensive service model, but they bear watching. If expense growth continues to outrun margin growth, Lube Heavy Firms’ ROCE advantage will narrow.

The Steadiest Hand: C-Store Heavy Firms

C-Store Heavy Firms’ 15.7% ROCE doesn’t lead the pack, but its year-over-year decline of just 0.4 percentage points was the mildest of any segment, and it was the winner of any of the segments by growing Adjusted EBIT, 5.4%.

The firms grew year-over-year margins by 1.4%, better than the national average and better than any of the other business segments. Both volume and margin gains drove gross profit dollar growth of 6.9%.

What sets C-Store Heavy Firms apart is cost discipline. Total operating expenses grew only 6.8%, the second-lowest rate after Propane Heavy Firms, meaning gross profit growth slightly outpaced expense growth. This is the only segment where the GPD-to-OpEx growth relationship worked in its favor (see Figure 2). Within the expense categories, C-Store Heavy Firms managed to reduce land and building lease costs by 6.4% and held G&A growth to 8.5%. Professional fees declined 6.7%. Even payroll, the largest single expense category, grew only 5.6%, well below the national average increase of 6.6%.

Figure 2

The capital employed as a percentage of assets is also the heaviest 80.1%, indicating C-Store Heavy Firms are more reliant on funding their balance sheets with capital that costs them (interest bearing debt and owners’ equity) and less able to use other people’s money (often accounts payable). This large capital employed base is what keeps ROCE below Lube Heavy Firms despite strong earnings performance; C-Store Heavy Firms simply requires more invested capital per dollar of operating profit.

Lagging: Wholesale Fuel Heavy Firms

Wholesale Fuel Heavy Firms’ gallons increased by 6.1%, more than the national average, but CPG margins declined 3.7%, the only decline among our four business segments. A bright spot was an increase in Other Operating Income of 20%. The net result was gross profit dollar growth of only 4.8%, below the national average.

Meanwhile, expenses rose faster. Total operating expenses grew 7.9%, creating the widest negative gap between GPD and OpEx growth of any segment that maintained positive gallon growth (Figure 2). The pain was largely concentrated in payroll, with payroll dollars increasing 10.5% and payroll as a percentage of gross profit increasing 1.8 percentage points.

The result: Adjusted EBIT fell by 5.6%, income from operations declined 16.6%, and ROCE dropped by 3.9 percentage points, the steepest decline of any segment. Making matters structurally more difficult, capital employed grew by 25.0%, the largest percentage increase of any segment, meaning even flat earnings would have driven ROCE lower. Wholesale Fuel Heavy Firms’ 2025 14.9% ROCE is the weakest of the four business segments.

Under Pressure: Propane Heavy Firms

Propane Heavy Firms posted the second-highest ROCE at 15.9%, but the trajectory is concerning. This segment suffered the second-steepest ROCE decline at 3.8 percentage points, and the underlying data suggests the problems are deepening.

Propane Heavy Firms was the only segment to lose volume, with total gallons declining by 1.3%. Per-gallon margins improved by 2.5%, but on a declining volume base, this translated into essentially zero gross profit dollar growth. As the GPD vs. OpEx Growth chart starkly illustrates (Figure 2), Propane Heavy Firms’ blue GPD bar is barely visible.

With capital employed growing by just 1.8%, the flat GPD might have been survivable, if expenses had cooperated. They did not. While total operating expenses grew by just 4.1% (the lowest rate), that still outpaced the negligible GPD growth by an enormous margin in percentage terms. Income from operations plummeted 23.6%, the worst decline of any segment.

The expense detail reveals specific pressure points. Health insurance surged 44.1% and employee benefits are already the highest in the study at 4.2% of gross profit. Vehicle repair and maintenance rose 10.8%, reflecting the wear and tear of a delivery-intensive model. Fuel costs for company vehicles fell 12.7%, providing one of the few bright spots.

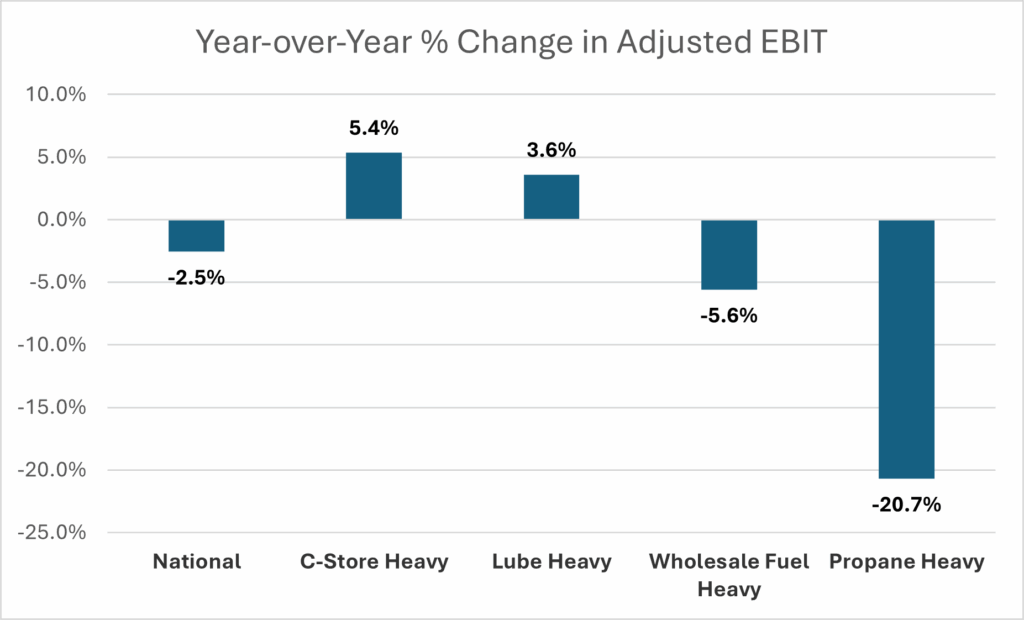

The earnings damage was severe: Adjusted EBIT fell by 20.7%, by far the largest dollar decline of any segment. See Figure 3.

Figure 3

Key takeaways

2025 results show that focused petroleum business models outperformed the national average on ROCE, but every segment still saw year-over-year deterioration, making the drivers of that decline the real story.

- Lube Heavy Firms led (19.9% ROCE) on the back of strong blended margin expansion and volume growth that lifted gross profit dollars, yet their advantage is vulnerable because operating expenses (especially payroll and “all other”) and capital employed rose even faster.

- C-Store Heavy Firms delivered the most resilient performance (15.7% ROCE with the smallest decline) because gross profit growth slightly outpaced operating-expense growth, reflecting unusually strong cost discipline even as they carry a heavier capital-employed burden that caps ROCE.

- Wholesale Fuel Heavy Firms illustrate how volume alone is insufficient: falling margins, faster expense growth (notably payroll), and a surge in capital employed compressed earnings and drove the steepest ROCE drop.

- Propane Heavy Firms highlight the risk of a delivery-intensive, shrinking-volume year—modest margin gains could not offset flat gross profit dollars and benefit/maintenance cost pressure, leading to a sharp earnings decline despite low overall OpEx growth.