2025 was a strong year for general contractors in a Study Group, with meaningful improvements across virtually every profitability metric. Here is a look at how these firms performed as a group, where they excelled, and where the road ahead presents some challenges.

Revenue and profitability: a year of operational improvement

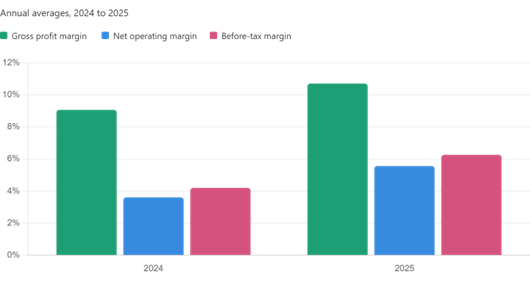

Revenue grew 4.1% year over year, a solid but measured gain. What makes 2025 stand out is not the top-line number; it is how much more of that revenue the firms kept. Gross profit margin expanded from 9.1% in 2024 to 10.7%, a gain of 1.6%, driven by improved project mix and better management of subcontractor costs. Before-tax profit margin climbed from 4.2% to 6.3%, a 49% increase in earnings efficiency. These gains collectively signal that 2025 was a year of operational improvement, not just revenue volume. See Figure 1

The net operating margin of 5.6% is the highest that Study Groups general contractors have recorded in the past 4 years. One notable detail in the 2024 data: net operating margin actually dipped to 3.6% that year despite healthy gross margins, suggesting that overhead costs were absorbing a larger share of revenue. The recovery to 5.6% in 2025 indicates firms either gained better control of their overhead structure or benefited from higher-margin project types moving through the system.

Figure 1

Balance sheet: strong financial health

The financial position of the Study Groups general contractor firms is notably healthy. The debt service coverage ratio (EBIT to annual debt service) came in at 6.7x, up from 6.3x in 2024, reflecting that this group of firms carries very little funded debt relative to their earnings. Funded debt accounts for only about 3.3% of total assets, and the funded debt-to-equity ratio is just 0.14x. These are not leveraged-up balance sheets, and these firms are largely trade-financed operations, with liabilities predominantly composed of accounts payable and billings in excess rather than bank debt.

Return on equity reached 88.9%, up from 85.6% in 2024. The high ROE is partly a function of the asset-light model and the financial leverage that comes from trade payables, so it should be read in that context rather than as evidence of extraordinary equity efficiency on its own. Still, it reflects a group generating high net income relative to shareholders’ capital.

The cash cycle tightened from 17.1 days in 2024 to 15.3 days in 2025, and the collection period improved modestly from 75.3 days to 73.9 days. Top-quartile firms in the group are actually operating with a negative cash cycle, meaning they collect from clients before paying their subcontractors, which is a meaningful competitive and liquidity advantage.

The forward-looking concern: backlog is contracting

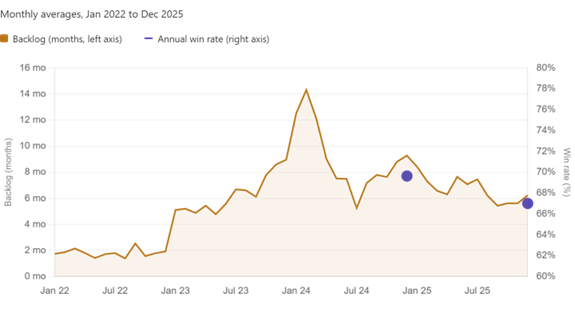

Despite strong 2025 results, the most significant concern heading into 2026 is the steady decline in backlog. The average backlog shrank from 7.7 months in 2024 to 6.4 months in 2025, a 16.5% drop. Stepping back further, Study Groups’ firms reached a backlog peak of 14.3 months in early 2024, reflecting the post-pandemic construction boom. The compression since then has been substantial, and the current 6.4-month figure, while still within a workable range, represents meaningfully less forward revenue visibility than firms enjoyed just 18 months ago.

Win rate also declined slightly, from 69.6% in 2024 to 67.0% in 2025. Neither number is alarming in isolation, but the combination of declining backlog and a softening win rate suggests firms will need to prioritize business development and bidding activity to sustain 2025 revenue levels into 2026. The backlog chart in Figure 2 tells a clear story. The surge through 2023 and into early 2024 reflected the post-pandemic construction boom. The peak in February 2024 at 14.32 months has given way to a gradual normalization, and pipeline replenishment is now the primary operational priority for 2026.

Figure 2

Macro environment: headwinds and tailwinds

Though not focused on commercial projects, housing building permits still provide valuable information on trends. Housing building permits totaled around 1,455,000 units in December 2025, down roughly 23% from the January 2022 peak, then declined again to 1,386,000 in January 2026. This suggests softness that will likely limit new residential project development in the near future. The 10-year Treasury, although it has pulled back from its 2023 highs, still averaged in the mid-4% range throughout 2025, keeping financing costs high for owners considering new construction. Construction materials price inflation was at 6.2% in 2025, a notable rise after a multi-year plateau following the post-COVID price spikes. On the positive side, total construction spending has increased by more than 21% since January 2022, and construction employment reached 8.28 million workers, up over 8% during the same period.

Quartile spread: the gap between leaders and laggards

One of the more striking findings in the Study Groups data is the performance gap between top and bottom performers. Gross profit margin at the top quartile is 16.8%, compared to 5.2% at the bottom quartile, an 11.6 percentage-point spread. Net operating margin shows a similar gap: 11.2% for top performers versus 1.1% for the bottom quartile. Win rates range from 45% at the low end to 84% at the top, and top-quartile firms carry over 10 months of backlog versus 3.8 months for those at the bottom.

Bottom line

General contractors in this peer group ended 2025 in a meaningfully better financial position than 2024, with stronger margins, healthier balance sheets, and improved cash management. The challenge for 2026 is that the favorable conditions driving profitability improvement, strong project flow, and favorable mix, are colliding with a backlog that has shrunk considerably from its peak. The firms that will navigate 2026 best are those investing now in business development, bid selectivity, and the operational discipline that separates the top quartile from the rest.